What a Difference a Year Makes

So what's the trend?

Last year around this time, we were ONE year into the Fed's interest rate hikes. You can see that we're about even with where interest rates were last year - 6.75%, but with the latest Jobs Report today, the Fed is walking back their prediction of 3 rate cuts this year. Oh, yea, good Ole' Jerome is tap dancing around so he doesn't wreck the stock market, but unless there's some crazy reduction in jobs numbers, the likelihood is One or NONE for the balance of the year. That's going to put a cooling effect on the buy side of the market.

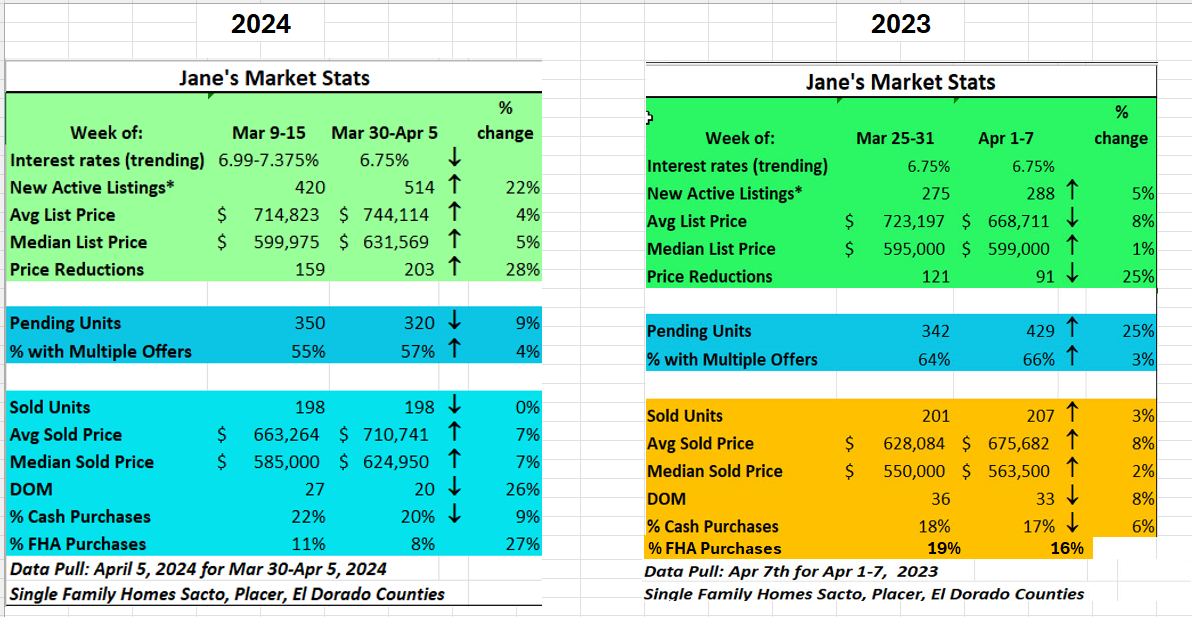

You can see that there's twice as much activity this early in the season as last year at this time. My stager is telling me she's staging a lot of houses for beneficiaries whose parents passed away. There's also still movement to EXIT California. Anecdotally, people are chatting about stubbornly high interest rates, the effect the lawsuit will have on sales, and the long term effects of low inventory.

That low inventory still drives the prices up - LAST year we saw an average sold price of $675k and this year $710k - raw numbers $35k more which equates to a 5% increase which BTW is considered NORMAL appreciation. It's just that most people didn't get a corresponding 5% increase in pay.

Half as many FHA buyers as last year means that many first time home buyers are not able to get into the market. They are PRAYING and HOPING that the lawsuit brings prices down so they can afford to buy. It's also an Election year for whatever that's worth. Let's see the Fed lower interest rates into the low 5's for mortgages and then we'll see some of the sellers calculate they can justify trading a 3% to a 5% loan. There's more cash buying homes too but it's marginal.

Is it doom and gloom? Not really. If you're a middle class buyer, you build WEALTH by being a home owner. Building equity by regular price appreciation, paying down the equity with each payment, and getting tax benefits for owning over renting has always been a magical combination to building wealth. For Sellers, today things are still looking favorable for selling - Do you want to know what your home is worth? I'm happy to show you what you could sell for. Further out this summer, I think anyone that tells you they know what's going to happen is simply blustering for publicity. There's simply too many major forces at work that are not stationary.

Hope you have a great weekend!

BTW - We closed on the home in Auburn where I represented the seller and got $15,500 more than asking and they EXITED California to Georgia! Congratulations to Ann & Darrick!!!!! It was a multiple offer situation. The lender fell down in their duties and I was project managing it right up until the day after Easter!

Hope you all had a nice Easter!

I spent mine down in Escondido with my granddaughter! I really like the grand parent thing! :)

Enjoy the weekend! If you have any questions or comments, feel free to send me an email or reply to this post (it just goes to me).

Jane